Many Australians feel a growing sense of frustration when they open their annual superannuation statement. You see the fees, you see the “balanced” returns, but you have no idea what’s actually happening inside the “black box” of your industry or retail fund. If you’ve ever felt that your retirement savings are stuck in a slow lane managed by someone who doesn’t share your urgency, you aren’t alone.

A Self-Managed Super Fund (SMSF) offers a different path. It is a private superannuation fund managed by its members, now up to six people, thanks to recent regulatory changes. The value proposition is simple: total control and investment flexibility.

But here is the counter-intuitive truth: being your own boss in superannuation isn’t a hobby; it’s a job. In this guide, we’ll strip away the marketing fluff to show you the rewards, the risks, and the regulatory realities of taking the wheel.

You Are the CEO and the Compliance Officer

If you’re looking for a “set and forget” investment, stop reading now. An SMSF demands a CEO mindset. A common misconception is that hiring a high-priced accountant or administrator shifts the legal burden away from you. This is false. While you can outsource the paperwork, you cannot outsource the liability. As a trustee, you are personally and legally responsible for every decision the fund makes, even if you are acting on professional advice.

Responsibility Snapshot

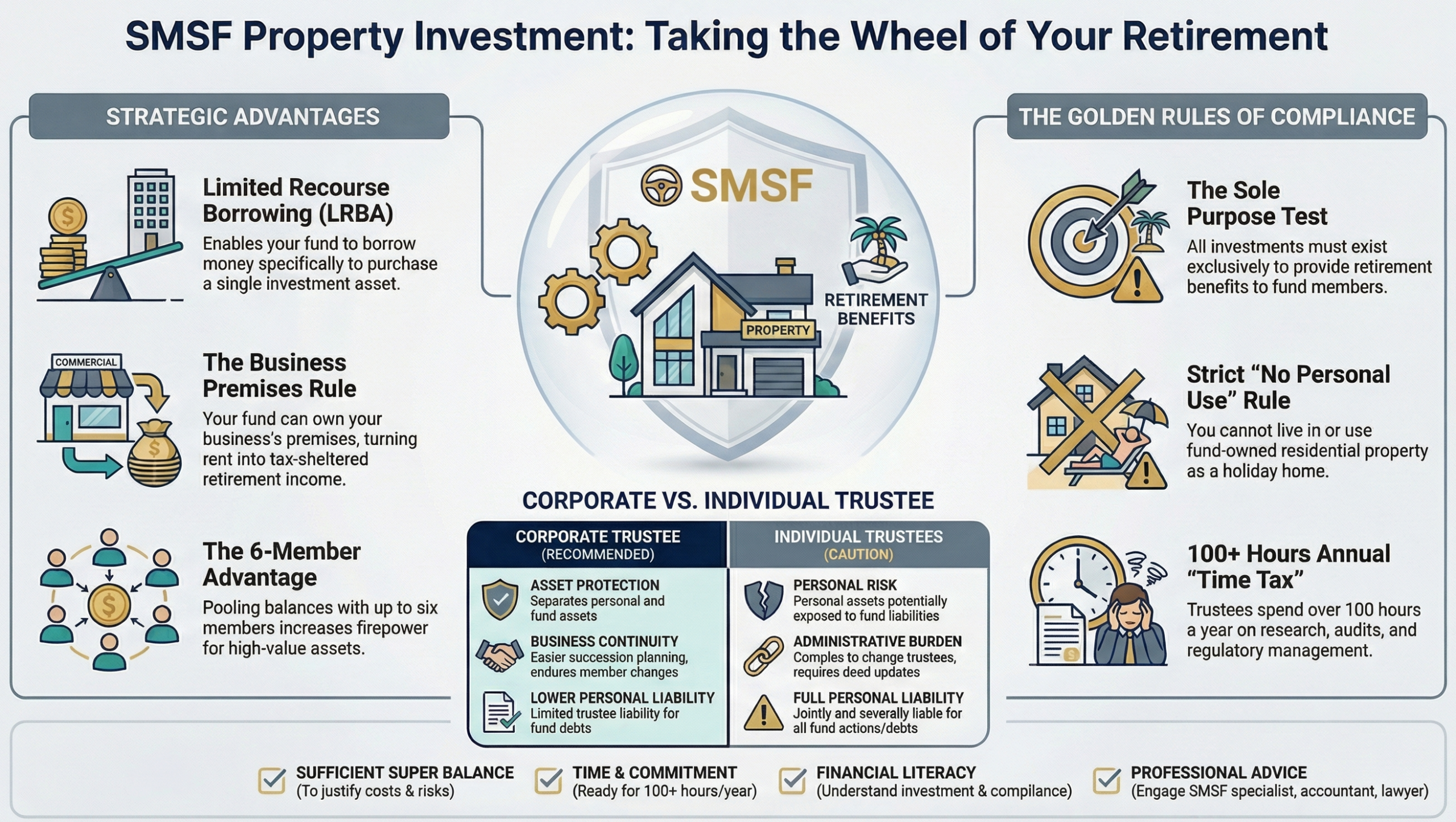

Investment Strategy: You must develop, maintain, and regularly review a strategy that suits the risk profile and retirement goals of all members.

The Sole Purpose Test: Every decision must pass one test: Is this exclusively for the purpose of providing retirement benefits to members?

Legal Compliance: You are responsible for record-keeping, lodging annual tax returns, and ensuring the fund adheres to complex ATO regulations.

The Power Takeaway: The buck stops with you. Whether it’s an administrative error or a bad investment, the ATO holds the trustees, not the accountants, accountable.

The “Time Tax” is Higher Than You Think

Traditional super funds handle the heavy lifting of administration for a fee. When you move to an SMSF, you trade those fees for your own time. Data from the SMSF Investor Report reveals that trustees spend, on average, more than eight hours a month, or over 100 hours a year, managing their fund. This includes researching assets, reviewing insurance, and overseeing the annual audit. If you aren’t prepared to treat your super like a part-time job, an SMSF may not be the right fit for your lifestyle.

The Missing Safety Net: A High-Impact Warning

One of the most critical differences between an SMSF and an APRA-regulated fund (industry/retail) is the safety net. If an industry fund loses money due to fraud or theft, members may be eligible for government compensation. SMSFs are not covered by these schemes. There is also a significant nuance regarding the Australian Financial Complaints Authority (AFCA):

- Internal Disputes: You cannot use AFCA to resolve disputes between members or trustees. These are often settled in court.

- Third-Party Disputes: You can still lodge complaints with AFCA against third-party financial firms (like brokers or advisers) that provided your fund with services.

Essentially, you are the primary line of defense for your own retirement nest egg.

Why “Cheap” Setups Backfire (Corporate vs. Individual)

The biggest mistake new trustees make is attempting to minimize costs on “Day 1” by choosing an Individual Trustee structure. While it’s cheaper to set up, it creates a “re-titling nightmare” later.

| Feature | Individual Trustees | Corporate Trustee (Recommended) |

|---|---|---|

| Upfront Cost | Lower (no company setup fee). | Higher (requires ASIC registration). |

| Succession Planning | High Complexity. If a trustee dies, assets must be re-titled and mortgage docs re-written. | Seamless. The company owns the assets; you simply change the directors. |

| Asset Protection | Lower; assets are held in individual names. | Higher; clear legal separation from personal assets. |

| Lender Preference | Many banks find these structures “messy” for loans. | Preferred by lenders for long-term stability. |

The Strategy: Using a corporate trustee ensures the fund remains a constant legal entity, protecting you from massive legal costs and administrative headaches during life events like relationship breakdowns or deaths.

Property Investment: The Strategic Advantage

For Pinpoint Finance clients, the primary draw of an SMSF is often direct property. There are two “power moves” here:

The Business Premises Rule: Your SMSF can own your business’s premises. Your business pays rent to your SMSF at market rates. This rent is a tax-deductible expense for the business and tax-sheltered income for the super fund.

Limited Recourse Borrowing Arrangements (LRBA): This allows your fund to borrow to purchase property. Because LRBAs are technically complex, navigating the lending landscape requires a specialist. Pinpoint Finance specializes in these structures to ensure your loan complies with the law from the start. For more information, read our guide on Unlocking Property Investment: The Ins and Outs of SMSF Loans in Australia.

The Warning: The rules are unforgiving. You must strictly adhere to the “No Personal Use” rule. You cannot live in a residential property owned by your fund, nor can you use it as a holiday house.

The Power of Pooling (The 6-Member Advantage)

A recent regulatory update increased the maximum number of SMSF members from four to six. This allows larger families or business partners to combine their balances, which has two massive benefits:

Increased Firepower: Pooling allows the fund to purchase higher-value assets (like a $1.5M commercial warehouse) that an individual could never afford.

Cost Efficiency: Many SMSF costs, like the annual audit, accounting fees, and the ATO supervisory levy, are fixed. By pooling six members, you split these costs six ways, significantly dropping the “per member” expense.

Summary Checklist: Are You Actually Ready?

The Result:

Checked 5/5? You’re ready to take the wheel.

Checked 3/5? You need professional advice before proceeding.

Checked 1/5? Stick with your current fund; the “Time Tax” will outweigh the benefits.

FAQ

What is the minimum balance to start an SMSF?

There is no legal minimum, but there is a “cost-effective” reality. Because of fixed audit and ATO fees, a small balance can be eaten alive by costs. The median balance for new funds as of 2022 was $264,000.

Can I use my SMSF to buy a home to live in?

Absolutely not. This is a major breach of the Sole Purpose Test. Using fund assets for personal housing or a holiday home can lead to the fund being declared non-complying, which carries heavy financial penalties.

What are the ongoing costs of an SMSF?

Expect to pay for an annual independent audit (required by law), accounting/tax services, and the annual ATO supervisory levy. If you have a corporate trustee, there is also an annual ASIC fee.

How many members can an SMSF have?

You can now have up to six members. Generally, all members must also be trustees (or directors of the corporate trustee).

Do I need a mortgage broker for an SMSF property loan?

While not legally required, standard residential brokers often cannot handle Limited Recourse Borrowing Arrangements (LRBAs). Pinpoint Finance specializes in these specialized loans, ensuring the complex trust structures satisfy bank requirements.

Taking the Next Step

An SMSF is a powerful vehicle for those who demand control and investment diversity. However, that power is balanced by a significant regulatory burden. You aren’t just an investor; you are the guardian of your own future. Is your current super fund working hard enough for you, or are you ready to take the wheel?

Contact Pinpoint Finance today for a discovery session. We’ll guide you through the complexities of SMSF investment lending and help you secure the pre-approval needed to build your property portfolio.