Why It’s More Important Than Ever to Refinance

Smart Australian professionals are discovering that refinancing their home loan is a strategic step toward long-term wealth creation rather than merely a tactical one in the fast-paced financial world of today. Refinancing your home loan is a great way to buy your next investment property or pay off your loan faster.

With the cost of living skyrocketing and fluctuating interest rates, it’s never been more important to ensure your home loan is working for you, not against you. This guide is tailored specifically for detail-oriented, career-focused Australians—like lawyers, accountants, and executives—who want to take control of their financial future without wasting time on outdated advice.

What Is Refinancing? A Quick Overview

Understanding the Basics

Refinancing is the process of replacing your current mortgage with a new one ideally with better terms, lower rates, or more suitable features. The primary reasons Australians refinance include:

- Lowering their interest rate

- Accessing home equity

- Consolidating debt

- Switching loan types or lenders

The Real-World Value of Refinancing

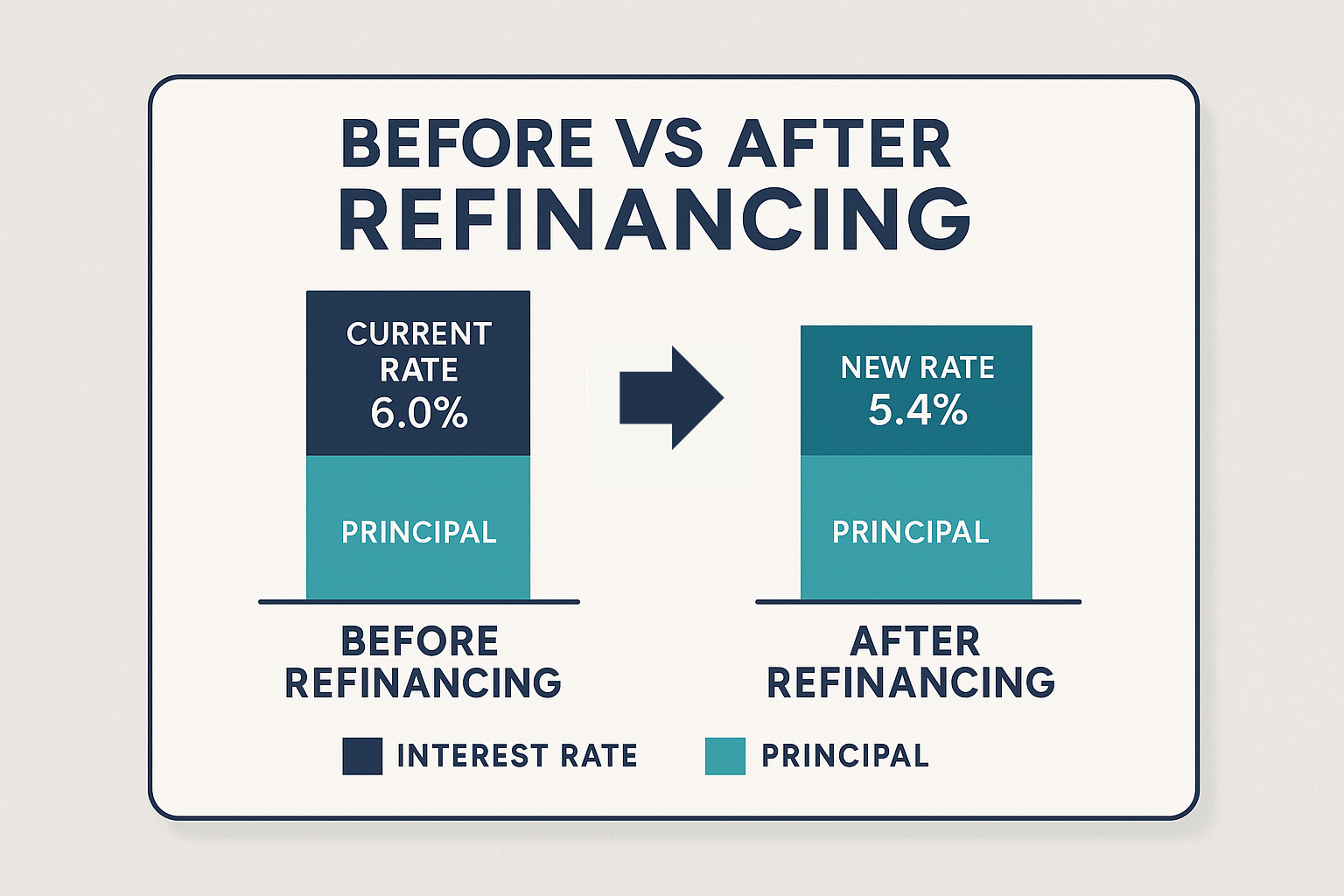

Let’s put it into perspective. If you’re on a $600,000 mortgage at 6.0% and the market is offering 5.4%, that 0.6% difference could mean saving over $180 a month. Over a 30-year loan, that’s more than $65,000 saved money you could reinvest or use to enjoy life.

When to Consider Refinancing Your Mortgage

Key Signs It’s Time to Refinance

- Your interest rate is no longer competitive.

- You’ve built up significant equity.

- Your fixed-rate term is ending.

- You want better features (like offset or redraw).

- You need to consolidate high-interest debts.

The Two-Year Rule and Extra Timing Advice

It’s a good idea to examine your home loan every two to three years, while there isn’t a hard rule. The market has most likely altered, even if your life hasn’t. Additionally, reviewing and refinancing can be as simple as sending a few emails and signing paperwork online with digital platforms like Pinpoint Finance.

Benefits of Refinancing in Australia

Lower Interest Rates = More Cash Flow

Reducing your interest rate by even 0.5% can significantly lower your monthly repayments. That frees up funds for savings, investing, or simply easing day-to-day financial pressure.

Unlocking Equity to Build Wealth

Many professionals are sitting on hundreds of thousands of dollars in untapped equity. Refinancing allows you to use that equity to:

- Buy your next investment property

- Renovate or upgrade your home

- Fund school fees or a new business

Access to Better Loan Features

Modern home loans offer powerful features like:

- 100% offset accounts

- Fee-free extra repayments

- Redraw facilities

If your current loan doesn’t offer these, it’s time to make a move.

The Seven-Step Refinancing Process (Pinpoint Finance Method)

At Pinpoint Finance, we’ve helped hundreds of ambitious Australians refinance their home loans with ease. Here’s our proven seven-step approach:

Step 1: Assessing Your Current Loan

We analyse your current mortgage, interest rate, fees, and remaining loan term to see if you’re actually getting value or if you’re paying more than you should.

Step 2: Clarifying Your Motivation

Are you refinancing to save money, release equity, or prepare for a future investment? Your motivation guides your loan strategy.

Step 3: Selecting the Right Loan Product

Based on your goals and financial profile, we recommend lenders and products with competitive rates, relevant features, and smooth processing times.

Step 4: Property Valuation

Your new lender will value your property to determine your equity and borrowing power. We manage this entire process for you.

Step 5: Unconditional Approval

Once your documents are in and your application is approved, you’ll receive an official letter of offer from your new lender.

Step 6: Documentation & Signing

Review and sign your new loan agreement. We guide you every step of the way, answering questions and ensuring no surprises.

Step 7: Settlement Day

Your new lender pays out the old loan, and your mortgage is officially refinanced. From here, you start enjoying the benefits of lower repayments, better features, or unlocked equity.

Common Refinancing Traps and How to Avoid Them

While refinancing can be financially rewarding, there are a few pitfalls that could cost you more than you save. Let’s explore how to sidestep these common issues.

Fixed Loan Break Fees

If you’re currently on a fixed-rate mortgage, breaking that contract early may come with substantial exit fees. These costs can range from a few hundred to several thousand dollars, depending on how long you have left on the fixed term and how much interest rates have changed since you locked it in.

Avoid It: Always ask your lender for a break cost estimate before you commit to refinancing. At Pinpoint Finance, we factor this into your savings analysis upfront.

Lender’s Mortgage Insurance (LMI) Pitfalls

LMI can’t be transferred between lenders. So if your new loan exceeds 80% of your property’s value, you may have to pay it again even if you paid it the first time.

Avoid It: We often order a desktop valuation to verify that your property has increased in value enough to avoid LMI a second time. This is a critical part of strategic refinancing.

Customer Retention Offers – Worth It?

Once your current lender receives your discharge notice, they may try to lure you back with a last-minute discount or cashback.

Avoid It: Don’t get emotionally swayed by last-minute offers. Instead, ask, “Can you backdate this offer? If not, and if their revised offer still doesn’t match what you’re getting elsewhere, move forward confidently with the refinance.

Costs Involved in Refinancing a Home Loan

Refinancing isn’t free—but the costs are often outweighed by the long-term benefits. Here’s what to expect.

Application, Discharge & Valuation Fees

| Fee Type | Typical Cost |

| Discharge fee (old lender) | $150–$400 |

| Application fee (new lender) | $0–$600 |

| Property valuation | Free–$300 |

| Settlement or legal fees | $0–$500 |

Many lenders waive fees as part of special offers or cashback promotions. At Pinpoint Finance, we always aim to help you find a lender that keeps these costs minimal or covers them completely.

Exit Fees: Are They Still a Thing?

Exit fees were banned in 2011 for new loans. However, older mortgages may still include these charges, especially if fixed. Always double-check with your current lender.

Will Refinancing Actually Save You Money?

This is the question at the heart of it all.

How to Calculate Real Savings

Let’s take a real-world example. Suppose you currently owe $750,000 on a 25-year loan at 6.2%. If you refinance to a 5.6% interest rate:

- Monthly repayment drops by approx. $255

- Annual savings: $3,060

- 25-year total savings: Over $76,000

Even after factoring in upfront costs, the long-term gain is clear.

The Role of Loan Comparison Rates

The comparison rate includes both the interest rate and standard fees associated with the loan. It gives you a clearer picture of the real cost of borrowing.

Pro Tip: Don’t just look at the advertised rate check the comparison rate to avoid surprises down the line.

How to Know If Refinancing Is Right for You

Before jumping in, ask yourself three essential questions.

Ask These 3 Key Questions First

- Has your financial situation changed?

New job, baby, promotion? Any change in income or expenses could influence your loan options. - Are you staying in the property long-term?

If you plan to sell in under two years, refinancing might not provide a strong return on investment. - Will you actually save money?

Make sure your break-even point (costs vs savings) justifies the switch. We help you calculate this during our initial consult.

Digital Refinancing: How Pinpoint Finance Makes It Easy

At Pinpoint Finance, we understand that professionals like you don’t have time to chase paperwork or sit through confusing meetings.

Paperless Process for Busy Professionals

Everything we do can be completed online, from:

- Uploading documents

- Signing loan applications

- Scheduling Zoom consultations

Our streamlined approach makes refinancing a zero-hassle experience for clients like Georgia and Simon, who are juggling full-time work, parenting, and big financial goals.

Case Study: Georgia & Simon’s Refinancing Journey

Let’s put theory into practice with a real example based on our ideal client avatars.

Their Goals, Challenges, and Success

Profile: Georgia (lawyer) and Simon (accountant), both in their 30s with a combined income of $300,000. They own a home worth $1.3M and have a $750,000 loan.

Pain Points:

- Paying more than 6.0% on their loan

- No access to offset features

- Confused by competing offers

What We Did:

- Ran a home valuation (property valued at $1.35M)

- Matched them with a lender offering 5.45% with full offset

- Helped them unlock $150K in equity for their next investment property

- Entire process completed in under 30 days—all online

Result: Over $65,000 in savings and a new investment property secured within the same year.

Top Mistakes to Avoid When Refinancing in 2025

Even experienced borrowers can fall into common refinancing traps. By staying informed, you can avoid unnecessary costs and delays.

Overlooking Fees

Borrowers often get dazzled by lower interest rates without factoring in the full cost of refinancing. Hidden charges like valuation fees, discharge fees, and application costs can eat into your savings if you’re not careful.

How to Avoid It: Ask your mortgage broker for a side-by-side comparison of your current loan and any potential new loans, including all costs.

Not Reviewing the Fine Print

Some low-rate loans come with rigid conditions, limited redraws, no offset accounts, or severe break costs on fixed rates.

How to Avoid It: Make sure the new loan has features that match your lifestyle, not just a shiny rate. Ask about flexibility, early repayment options, and associated fees.

Waiting Too Long to Act

Timing matters. Many borrowers lose money simply by procrastinating. If you suspect you’re paying too much, the best time to review your loan is now.

How to Avoid It: Set a reminder to review your mortgage every two years or sooner if your financial situation changes.

How Refinancing Fits into a Bigger Wealth Strategy

For professionals like Georgia and Simon, refinancing isn’t just about short-term savings it’s a gateway to financial growth.

Property Portfolio Planning

Accessing your home equity through refinancing can help you:

- Fund a deposit for an investment property

- Renovate to increase property value

- Diversify your assets without needing to sell

This is how many Australians build intergenerational wealth, one refinance at a time.

Using Equity as a Lever

Let’s say your home is now worth $1.5 million and your mortgage is $900,000. That means you’ve got $300,000 of usable equity (80% of your property value minus your current debt). This can be leveraged to:

- Buy your next home without selling

- Start a business

- Fund your children’s education

Pinpoint Finance helps you structure this equity efficiently so it works in your favour, not the bank’s.

Choosing the Right Mortgage Broker (Why It Matters)

Refinancing is complex. You want a partner who understands your goals, respects your time, and knows the market inside out.

DIY vs Professional Help

While it’s possible to research and apply for loans on your own, many professionals quickly find that comparing interest rates and reading PDS documents becomes a time sink. Worse still, you could miss better offers or critical loan conditions.

What Makes a Broker Like Pinpoint Finance Stand Out

- Award-winning service (14+ industry accolades)

- Fully digital experience perfect for busy professionals

- Transparent, tailored advice

- A deep understanding of your goals, lifestyle, and constraints

At Pinpoint Finance, you’re not just another loan number. You’re a client with ambitions, and we’re here to help you realise them.

FAQs About Refinancing in Australia

1. How often should I refinance my home loan?

Every 2–3 years or when there’s a significant change in your financial situation or the market.

2. Can I refinance an investment property?

Absolutely. In fact, many investors use refinancing to access equity and grow their portfolios.

3. What documents will I need?

Usually: recent payslips, ID, bank statements, current loan statement, and tax returns if you’re self-employed. Most of these can be submitted digitally.

4. Does refinancing hurt my credit score?

A small, temporary dip may occur due to the credit enquiry, but the long-term benefit of lower repayments often outweighs this.

5. Is refinancing worth it in 2025?

Yes, particularly if your interest rate is more than 0.5% above the current market. The savings can be substantial over time.

6. What if my current bank offers a better deal to stay?

That’s fine just ensure the offer is genuine and matches or beats the competition. A good broker can help you compare properly.

Your Next Steps Towards Financial Freedom

Refinancing isn’t just about saving money it’s about taking control of your financial future. For professionals who are already stretched for time, the idea of reviewing home loans might seem like a hassle. But with the right guidance, it can be one of the smartest financial decisions you make this year.

Whether you’re looking to reduce repayments, unlock equity, or streamline your financial setup, Pinpoint Finance is here to make the process clear, easy, and rewarding.

✅ Ready to refinance smarter?

Book your complimentary consultation with Edwena and the award-winning team at Pinpoint Finance. Let’s build your future on your terms.